What Adaptive Reuse Projects Have Taught Us as a Custom Bifold Door Manufacturer

Adaptive reuse is reshaping cities. Across North America, office towers, warehouses, hotels, and industrial buildings are being converted into multifamily housing and mixed-use communities. These projects create exciting opportunities for architects and developers—but they also introduce constraints that standard building systems rarely anticipate.

Working as a custom bifold door manufacturer on these types of projects, we’ve seen firsthand how conversion work differs from new construction.

Existing buildings rarely behave like blank canvases. Structural grids, deep wall assemblies, aging façade systems, and historic preservation requirements all shape what is possible. Openings that appear straightforward on paper often prove irregular or constrained once construction begins.

Because of this, adaptive reuse projects tend to shift the role of building products. Instead of simply selecting a standard system from a catalog, design teams often need components that can be engineered around existing conditions.

One of the recurring challenges we see involves activating existing building edges. Many older offices or industrial buildings were designed with sealed or limited openings on the ground floor. In residential conversions, however, developers increasingly want these areas to feel open and connected—to support amenities, shared spaces, or retail uses.

Large operable openings, including bifold systems, are sometimes used to help transform these previously closed façades into flexible indoor–outdoor environments. In practice, integrating these systems into existing structures often requires careful coordination between architects, engineers, and manufacturers.

Another observation from working in adaptive reuse is how much risk management influences specification decisions. Conversion projects already carry uncertainty related to structure, code compliance, and existing conditions. As a result, architects tend to rely heavily on manufacturers who can provide clear documentation and collaborate early in the design process.

Technical resources—BIM models, CAD details, performance data, and engineering consultation—often become just as important as the product itself. They help design teams evaluate feasibility before issues appear during construction.

We’ve also noticed that the most successful adaptive reuse projects tend to focus on reimagining how existing spaces function, rather than simply subdividing them into units. Daylight access, flexible amenity areas, and connections to the street or courtyard often become defining features of the redevelopment.

In those contexts, façade openings and operable systems can play a small but meaningful role in shaping how residents experience the building.

For manufacturers involved in adaptive reuse work, the takeaway is straightforward: these projects are less about selling products and more about understanding how new systems integrate with old buildings.

Every conversion is different. Existing structures come with their own geometry, materials, and history. Supporting those projects requires flexibility, collaboration, and a willingness to adapt systems to the realities of the building itself.

As adaptive reuse continues to grow in urban development, manufacturers that approach these projects with a problem-solving mindset will likely find themselves contributing not just components—but solutions—to the evolving built environment.

Adaptive Reuse in Major U.S. Metro Areas (2010–2026)

Key National Indicators

~25,000 apartments were completed through adaptive reuse in 2024 alone, the highest annual level on record.

This was 50% more than 2023 and roughly double the 2022 levels.

About 181,000 additional apartments are currently in the pipeline nationwide.

Hotels produced ~37% of converted units, offices about 24%, industrial ~20%, and schools ~8%.

1. Adaptive Reuse Apartments Completed by Year (U.S.)

Estimated totals based on national datasets.

Year Units Completed

2010 ~4,000

2012 ~6,000

2014 ~8,500

2016 ~10,000

2018 ~13,000

2020 ~12,000

2021 ~20,000

2022 ~12,000

2023 ~16,000

2024 ~24,700

2025–2026* ~25,000+ per year projected *Estimates based on pipeline and recent delivery pace. https://www.bdcnetwork.com/home/news/55165996/adaptive-reuse-report-shows-55k-impact-of-office-to-residential-conversions

2. Largest Metro Markets for Adaptive Reuse (Recent Deliveries)

Major metros leading apartment creation from conversions.

City / Metro (2024) Units Delivered

Chicago 880

Denver 789

Philadelphia 761

Dallas 698

Manhattan (NYC) 588

Houston 372

White Plains NY 468

These figures reflect large conversion projects completed in those markets.

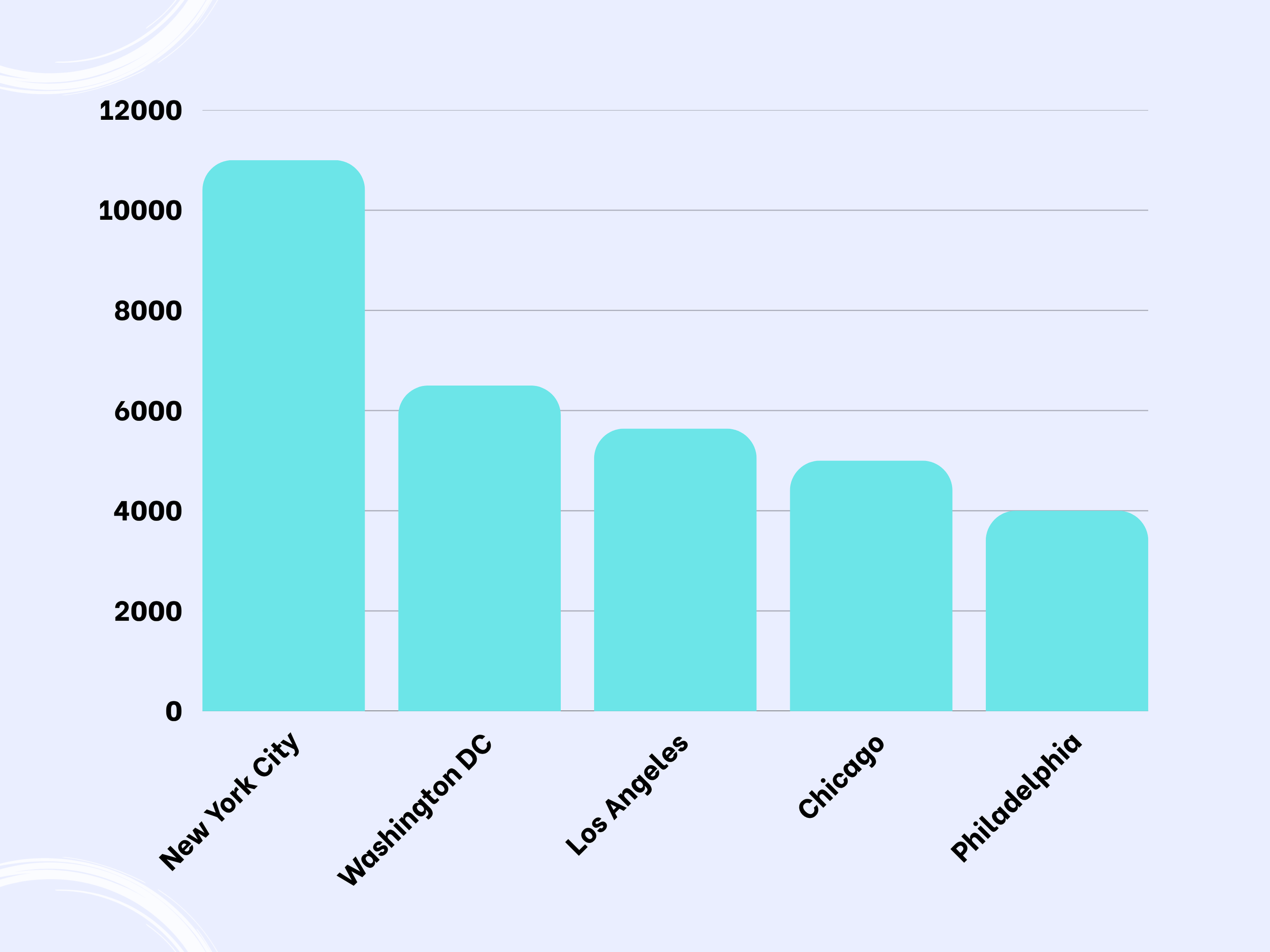

3. Largest Metro Pipelines (2025–2026)

Projects in planning or construction.

Metro Area Units in Pipeline

New York City ~11,000

Los Angeles ~5,640

Chicago ~5,000

Washington DC ~6,500+

Philadelphia ~4,000+

Denver ~3,000+

Atlanta ~2,000+

Dallas ~2,000+

Office conversions dominate the future pipeline.

Make it stand out

Whatever it is, the way you tell your story online can make all the difference.

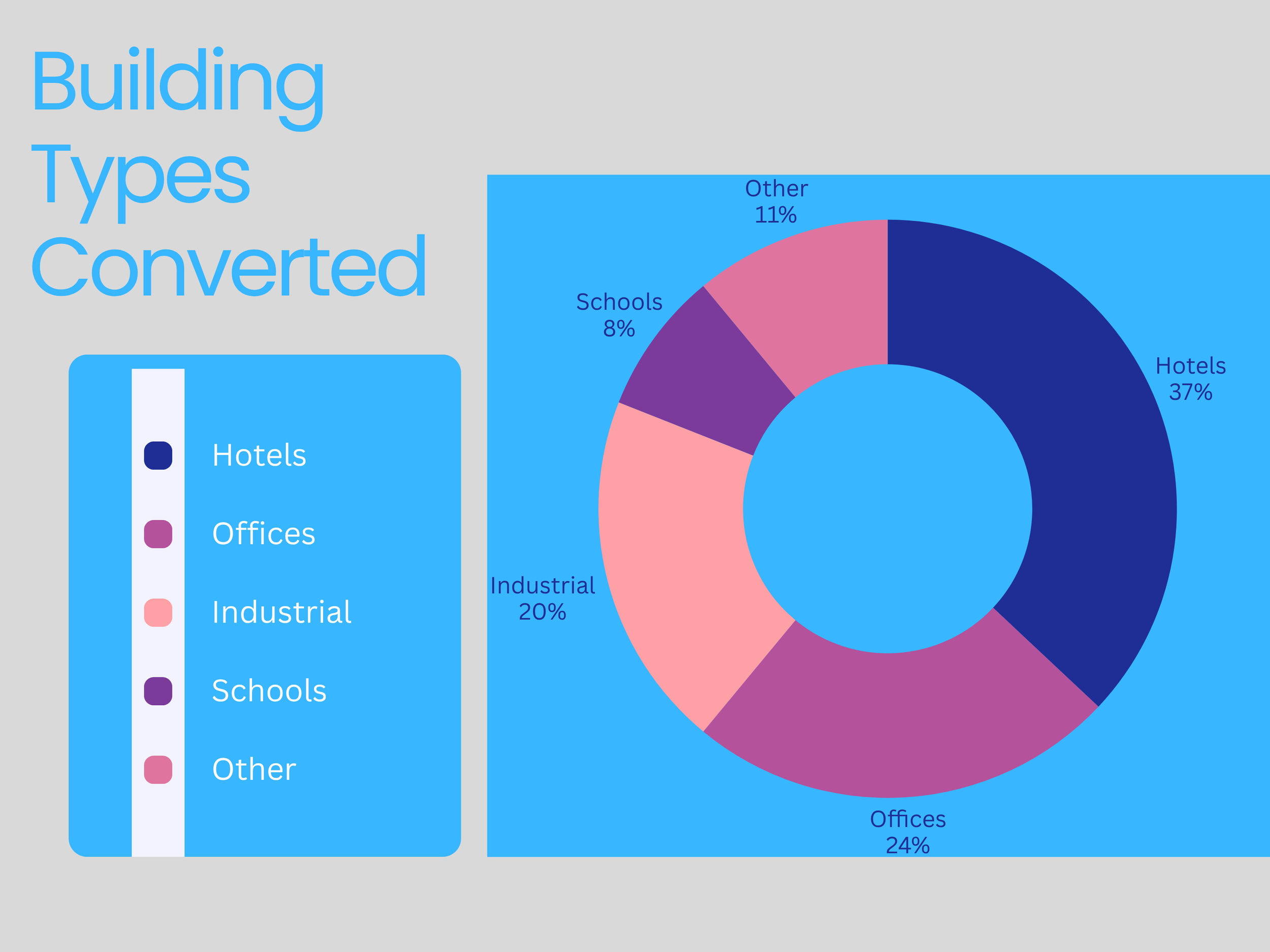

4. Building Types Converted (2024 Share)

Type of Building % of Units

Hotels 37%

Offices 24%

Industrial 20%

Schools 8%

Other 11%

Make it stand out

Whatever it is, the way you tell your story online can make all the difference.

Hotels and offices dominate because they already contain:

plumbing cores

repetitive floor plates

central urban locations.

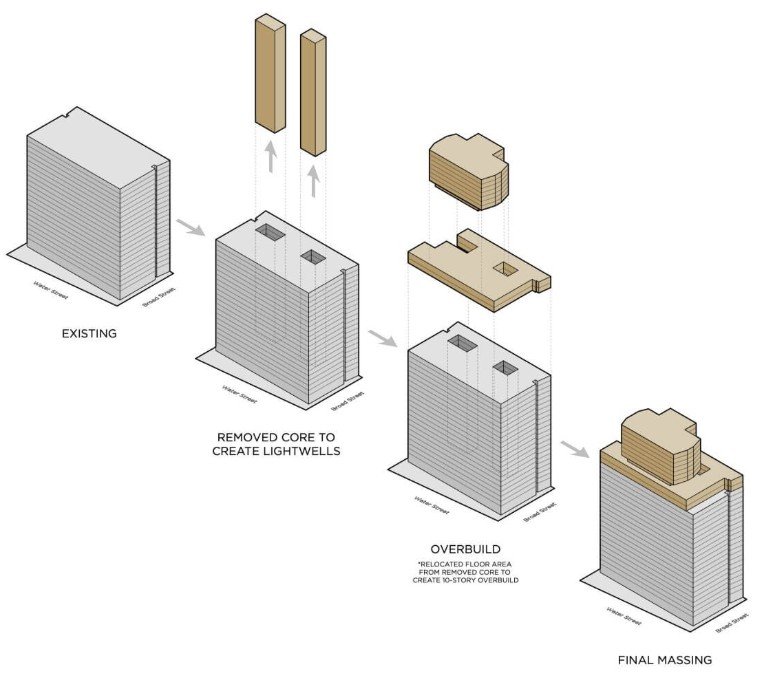

MA massing diagram shows the modifications CetraRuddy made to the former office building. The architects cut two light wells through the building’s bulk. The subtracted area was then added to the top of the building. (Courtesy CetraRuddy) ake it stand out

Whatever it is, the way you tell your story online can make all the difference.

8. Structural Trends Shaping Adaptive Reuse

1. Office Vacancy

Remote work left millions of square feet of unused office space.

2. Housing Shortage

Cities increasingly see conversions as a fast supply solution.

3. Public Incentives

Cities such as Chicago, Denver, and Washington DC now offer:

tax abatements

zoning changes

conversion grants.

Key Insight

Adaptive reuse has shifted from historic preservation projects in the early 2010s to large-scale office-to-residential redevelopment in the 2020s.

The next wave will likely concentrate in downtown office districts built between 1970–2000, which are increasingly obsolete but structurally adaptable.

Timeline: Adaptive Reuse Housing Boom

Units created via adaptive reuse (national estimate)

Year

Units Created

2010

1,300

2011

1,400

2012

2,000

2013

2,500

2014

3,100

2015

3,700

2016

4,400

2017

5,200

2018

3,900

2019

3,900

2020

12,000

2021

20,100

2022

18,000

2023

22,000

2024

30,000

2025

45,000 (pipeline deliveries)

2026

~70,000 pipeline

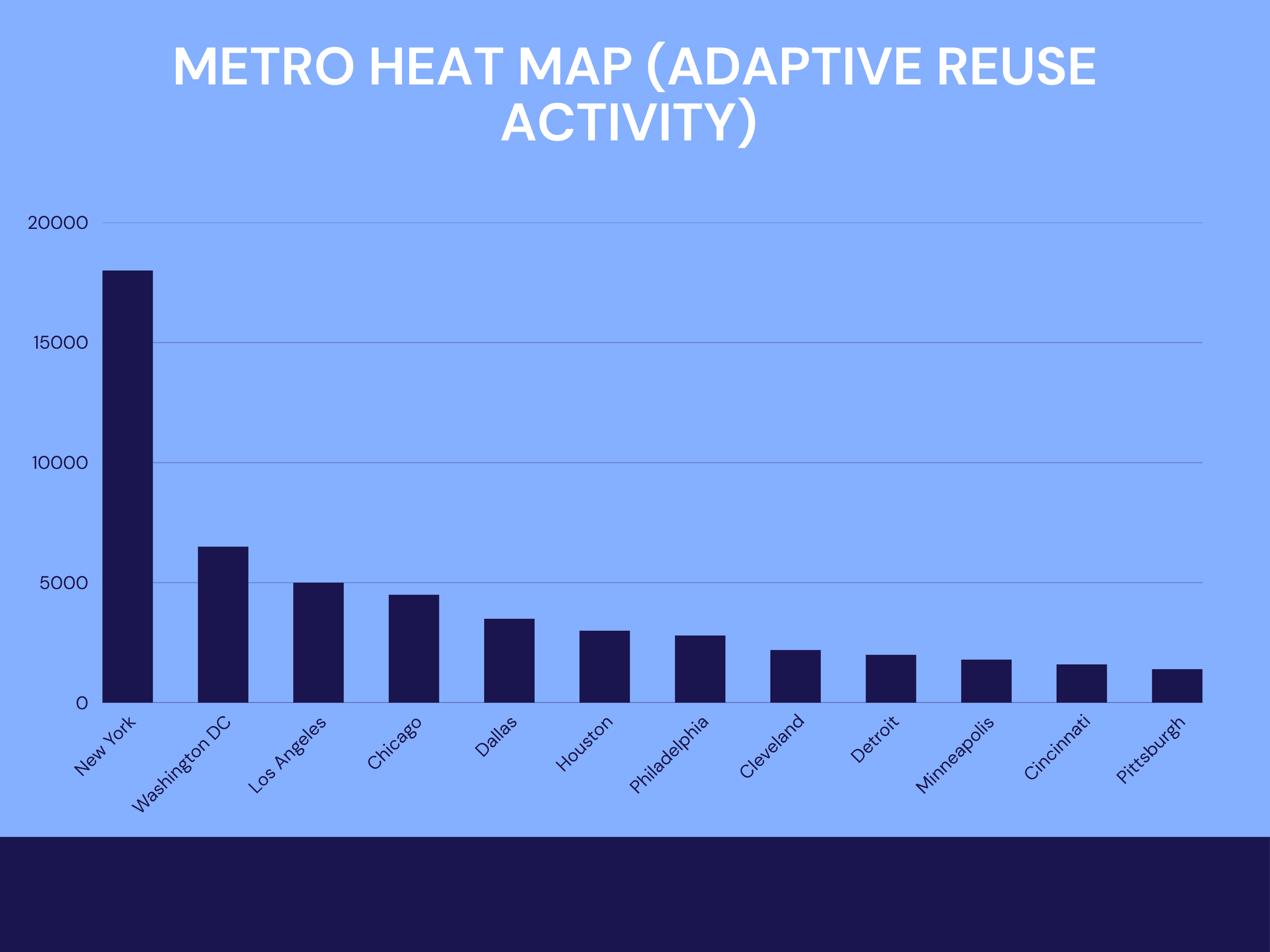

Metro Heat Map (Adaptive Reuse Activity)

Top metros by adaptive reuse multifamily units created or in the pipeline

Rank

Metro

Estimated Units (2010-2026)

Key Driver

1

New York

18,000+

office conversions

2

Washington DC

6,500+ pipeline

federal office surplus

3

Los Angeles

5,000+

DTLA adaptive reuse ordinance

4

Chicago

4,500+

historic loft conversions

5

Dallas

3,500+

downtown office towers

6

Houston

3,000+

office surplus

7

Philadelphia

2,800+

historic office conversions

8

Cleveland

2,200+

historic bank towers

9

Detroit

2,000+

industrial reuse

10

Minneapolis

1,800+

warehouse districts

11

Cincinnati

1,600+

office reuse

12

Pittsburgh

1,400+

historic office conversions

Cities like Manhattan, Dallas, and Houston have seen large tower conversions exceeding 300–600 units per building.

Make it stand out

Whatever it is, the way you tell your story online can make all the difference.